In this blog: When an Uber Eats, DoorDash, Instacart, or Amazon Flex driver hits someone in Atlanta, the insurance dispute can hinge on whether the driver was logged in, waiting for an order, picking up food or packages, making a delivery, or using the car for personal travel. These claims can involve personal auto insurance, platform-linked coverage, exclusions, app data, and competing insurer narratives.

A delivery driver is at fault for a crash, and now your pain has a corporate paper trail attached to it. The person behind the wheel was working through Uber Eats, DoorDash, Instacart, or Amazon Flex, and that detail can change the insurance investigation from a basic car wreck into a dispute over app status, delivery activity, exclusions, and layered coverage. The injured person gets the consequences first: the ambulance bill, the missed work, the calls from adjusters, the damaged car, the body that hurts worse the next morning. The companies get time to sort through policy language. That gap is where people can get taken advantage of, especially when an insurer acts certain about coverage before the delivery records have been reviewed.

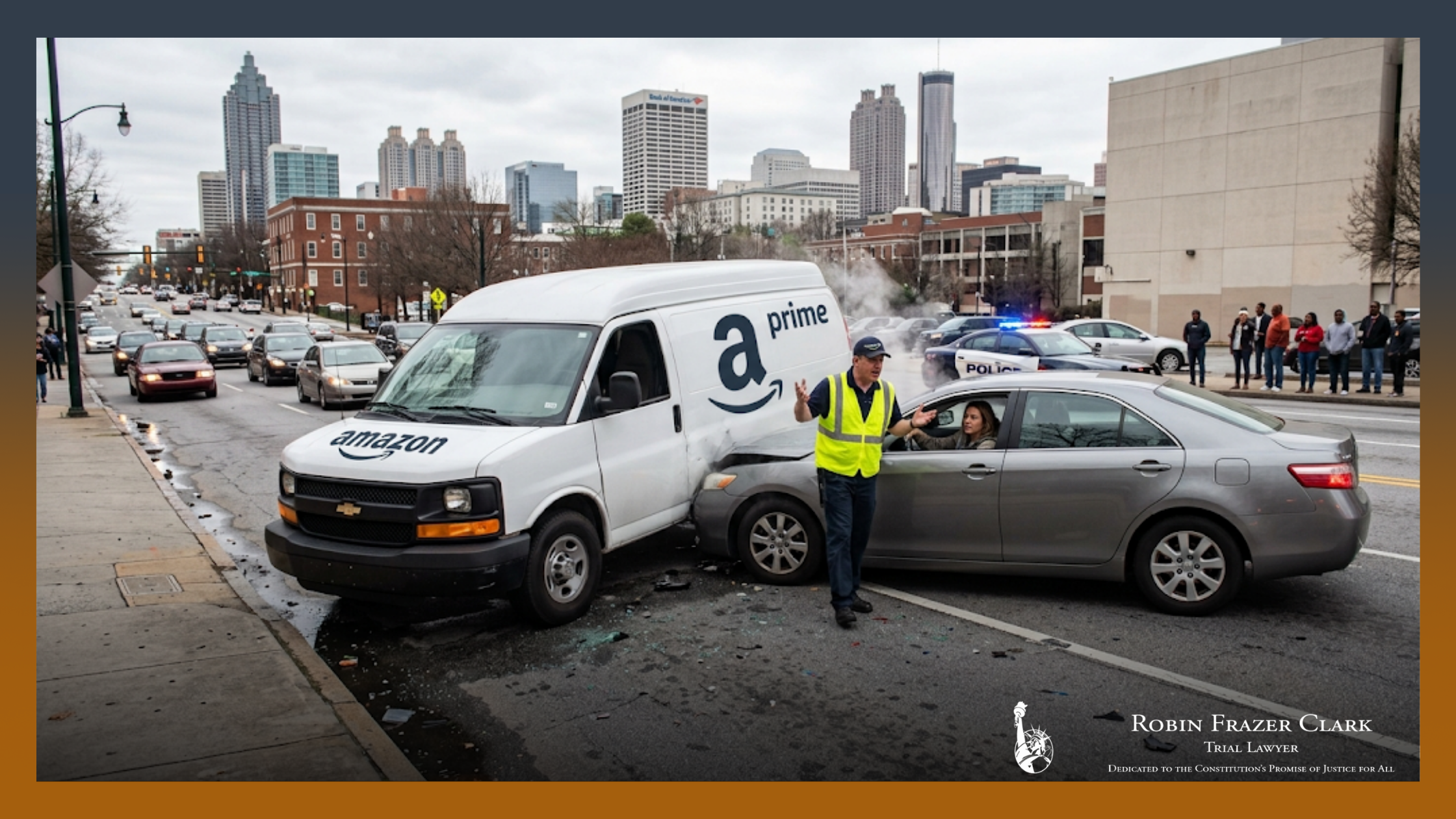

Why the Driver’s App Status Can Change the Claim

For delivery crashes, the driver’s status on the platform can change, which may affect which insurance coverage applies. A driver who’s logged out may be treated differently from a driver waiting for an order, heading to a restaurant, taking groceries to a customer, or delivering Amazon packages. That status isn’t always obvious from the police report. The answer may come from app records, GPS data, timestamps, pickup information, route history, delivery receipts, screenshots, and messages. Insurance companies know this, and they can use uncertainty to delay, deny, or reduce payment.

Layered Insurance Can Create a Fight Over Who Pays

“Layered insurance” refers to different policies that may apply at different times. A delivery driver may have a personal auto policy, while the platform may have additional coverage tied to a particular delivery stage. The dispute can center on whether a policy applies, whether an exclusion blocks coverage, and whether another insurer should pay first. Each platform writes its insurance promises in its own way. Uber Eats, DoorDash, Instacart, and Amazon Flex don’t all handle coverage the same way. The details of the delivery, the driver’s conduct, and the policy language can all influence the claim.

What You Save After the Collision Can Make or Break a Claim

Photos, videos, witness names, vehicle details, delivery bags, package labels, screenshots, insurer letters, medical records, and repair information can help show what happened. Treatment gaps, vague statements, missing app data, or early recorded statements can be used against an injured person. A lawyer can review the full set of facts before you accept an insurer’s version of events and provide context and guidance on how to protect your right to compensation. The sooner you get in touch with a legal team, the better. Talk to Robin Frazer Clark, P.C. About Your Atlanta Delivery App Crash If you’ve been injured by a delivery app driver, you don’t have to sift through confusing, layered insurance policies alone. Robin Frazer Clark, P.C. helps injured people in Atlanta push back when insurers try to minimize what happened. Call (404) 873-3700 for a free consultation to discuss your situation.

Delivery Driver App Collision FAQ

Yes, it may apply, but the answer depends on what the driver was doing at the time. A driver who had accepted an order and was heading to a restaurant may be treated differently from a driver waiting for an order or driving home after logging out. Uber Eats, DoorDash, Instacart, and Amazon Flex each have coverage rules tied to delivery activity, and insurers may fight over which policy applies.

A denial from the driver’s personal insurer doesn’t have to end the coverage review. Personal auto policies may exclude paid delivery work, which is one reason these crashes can become so frustrating for injured people. The next step may involve looking at the driver’s app status, the platform’s coverage, and any other insurance connected to the vehicle or delivery activity.

App data may show whether the driver was logged in, waiting for an order, traveling to a pickup, completing a delivery, or off the platform. That information can influence which insurer may be responsible. Screenshots, delivery receipts, GPS data, messages, and timestamps can help challenge an insurer’s attempt to place the crash outside coverage.